[ad_1]

MBW Reacts is a series of comments from the Music Business Worldwide team. These are our analytical (and sometimes dogmatic) reactions to recent major entertainment news stories.

“Big labels are losing market share on Spotify.”

So read the article headlines (or variations thereof) from the past few years.

The volume of “DIY” music uploaded to streaming services has skyrocketed, with the three major record labels (Universal Music, Sony Music, and Warner Music) seeing a small but consistent year-over-year decline in market share. increase.

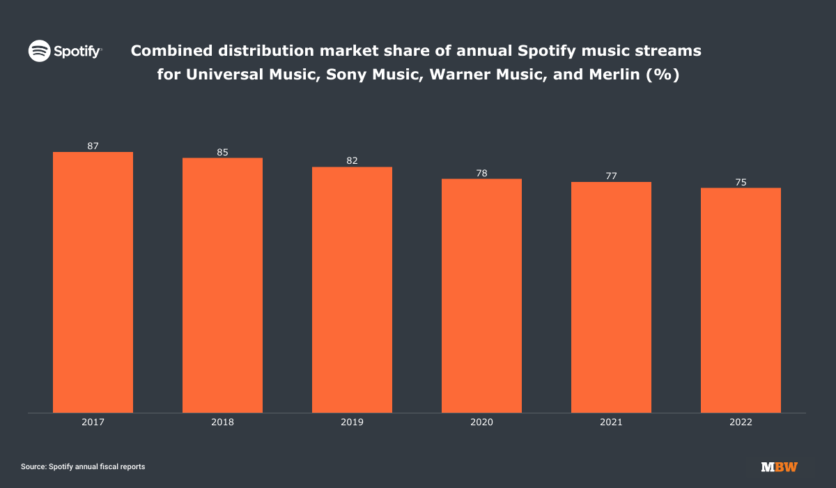

spotify, In the latest annual investor report, As MBW previously reported – Total “Major Plus Merlin” market share on that platform revealed 75% In 2022, it has decreased by 2 percentage points from the previous year.

This share has declined every year since 2017 when it was 12 points higher. 87%) than today, as seen above.

“majors-plus-Merlin” shares represent artists ultimately distributed through Merlin members, including the three major record labels (or their independent subsidiaries), or Beggars Group, among others. [PIAS]and secretly group.

(MBW clarified that Spotify’s non-major/Merlin figures above include distributors such as TuneCore, CD Baby, and DistroKid.

This spells bad news for the “major players” that have historically been compared with market shares that outperform other metrics, and for the industry as a whole.

This trend can be largely explained by the recent explosive growth of the independent, especially the ‘DIY’ artist sector.

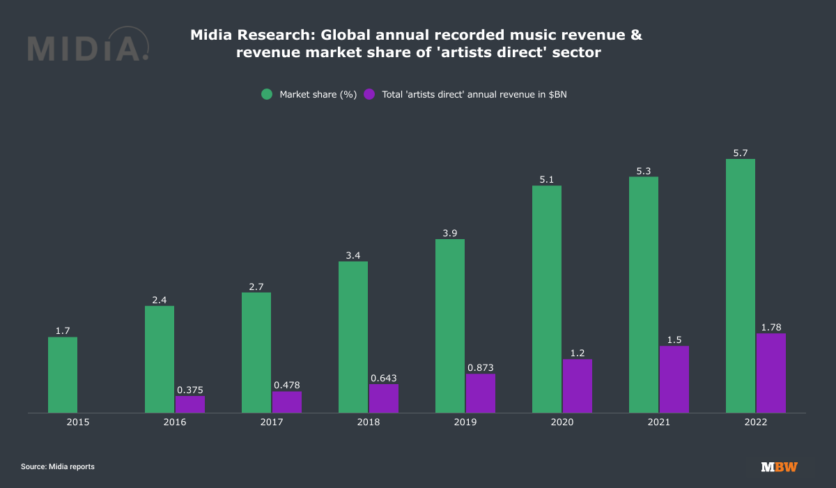

Globally, by 2022, MIDIA Report “Artist Direct” (self-released artists) held the market share of recorded music (the revenue standard for recorded music in the world). 5.7%.

This market share figure has increased every year since 2015. 1.7%. In other words, the market share of “Artist Direct” is more 3 times or more in 6 years.

On the other hand, the total revenue of the ‘artist direction’ sector, expressed in absolute terms, is quadruple From 2015 to 2022, $375 million (2015) what $1.78 billion (2022; MBW confirms this number with Midia to two decimal places).

On the one hand, this trend seems inevitable for majors given the rapidly increasing number of non-major distribution tracks uploaded each year.

And of course, it’s also worth noting that the majors have maintained double-digit growth rates. income Even though combined music streaming market share is declining, it is increasing each year.

On the one hand, this trend is also consistent with the changing perceptions of independent artists over the years. This shift may in some ways pose a greater threat to major artists.

In the past, artists with big ambitions were effectively forced to partner with record companies if they hoped to reach a wider audience on pre-streaming or iTunes (mass production of physical records was Not to mention prohibitively expensive). marketing, etc.).

currently represented by Major one It’s a pathway for aspiring career artists, but it’s not necessarily the most attractive option for everyone, given that independent pathways are more accessible than ever.

recent one MIDiA survey Hundreds of independent artists concluded that more than half would like to: [their] Scene” (53%); “Be successful as a touring artist” (51%); and “build a loyal fanbase of any size” (50%).

How many people ended up wanting to sign to a major label?

less than 1 in 6 – only 16%.

(9% would prefer to sign a label service deal instead, and 12% would prefer to sign with an independent label.)

Many indie artists, including some very successful, seem to have decided that the traditional major label route simply wasn’t for them.

To combat this, each of the three majors has, to this point, invested heavily in independent, artist-friendly alternatives to traditional labels.

- Universal Music have virgin music group,housing in-groovean independent distributor wholly acquired by UMG in 2019 for approximately $100 million;

- sony music has a label service department Orchard Even if beginningit got famous $430 million First half of 2021.and

- warner music includes the Alternative Distribution Alliance (ADA) and Level Music, a DIY distributor that competes directly with the likes of TuneCore and DistroKid.

In a relatively short period of time, these ‘label services’ businesses have gone from being just one line of business for big companies, from being relatively small to playing a central role in their future. It can be argued that

More than ever, more artists want to leverage the influence, global reach, and expertise of majors, but only on terms that allow them to maintain copyright ownership and relatively short-term licenses. Or you have to sign out only with a distribution agreement. .

As the mega-hit era may come to an end, this author believes the best path for majors to succeed To maintain streaming market share, alternatives to strong “name brand” labels should be used.

Leading label services business growing in market share and strategic importance

Nowhere has the importance of each major’s label services business to overall market share increased more than at Sony and The Orchard.

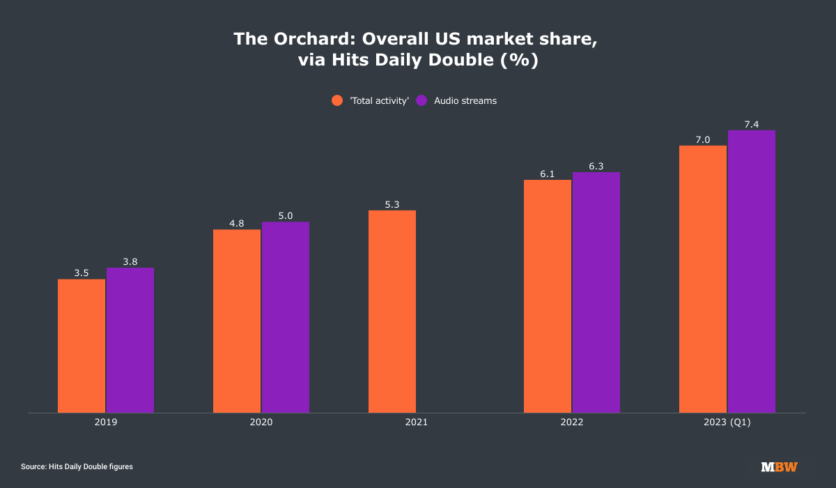

From 2019 to 2023, the latter’s market share in the US has doubled.

according to hit daily double The Orchard, with the success of artists such as RAYE and Bad Bunny, 7.0% Q1 US ‘Total Activity’ market share (‘Overall’), taking into account all releases.

That left it as Sony Music’s biggest entity at the time. Strong frontline labels such as Columbia (6.6%) and RCA (5.6%).

The growth in Orchard’s “total activity” US market share in recent years is a notable trend.

- In 2019, Hits reports. 3.5%;

- In 2020, 4.8%;

- Hit in 2021 5.3%;

- and in 2022 6.1%.

When it comes to “frontline” releases (i.e., online music published within the last 18 months), The Orchard claimed an even larger US “total activity” market share in Q1 2023. 8.3%say hit.

Essentially, organizations like The Orchard are giving artists like Bad Bunny, arguably the biggest artist in the world at the time of this writing, this while maintaining a contract with an independent label (Rimas Entertainment). Provides the ability to join major Sony Music. .

In other words, an internal label services company like The Orchard allows superstar-level artists to access major frontline label resources (financing, marketing, digital, radio, PR, etc.) without having to sign a traditional recording. dozens of departments in the contract.

For Bad Bunny, at Rimas Entertainment, Signed a label-wide deal with Orchard In 2021, the artist generated more streams on Spotify than any other artist in the last year. This has been a huge boon to Sony’s market share.

With a renewed focus on the independent artist and label segment of the music business, it’s no surprise that Universal and Warner’s label services companies will eventually overtake traditional labels, given enough time. maybe.

face the future

If majors continue to lose market share to DIY artists on Spotify and other music streaming platforms, it won’t come without a fight.

New times call for new business practices, and to their credit, major labels have taken some truly historic and groundbreaking steps in recent years to create a more just future.

New major label deals are also changing, and depending on the size and influence of an artist, a specific deal that would have been rarely seen in the physical era is now being offered: Artist retains ownership. License agreements, 50-50+ profit share, full creative control and more.

The major record companies always have a place, but as the dynamic shifts, their premium front-line labels can only take Universal, Sony and Warner so far.

In a world where the long tail is king and superstar artists aren’t as popular as they used to be, the world of label services and distribution is where majors must focus to maintain their market share throne.global music business

[ad_2]

Source link